Cost of Living Support for Real Life

Practical ideas, tools, and financial guidance to help reduce pressure, strengthen financial confidence, and move forward with greater clarity.

This page is designed to help you review the areas that matter, take practical action, and build financial confidence in everyday life.

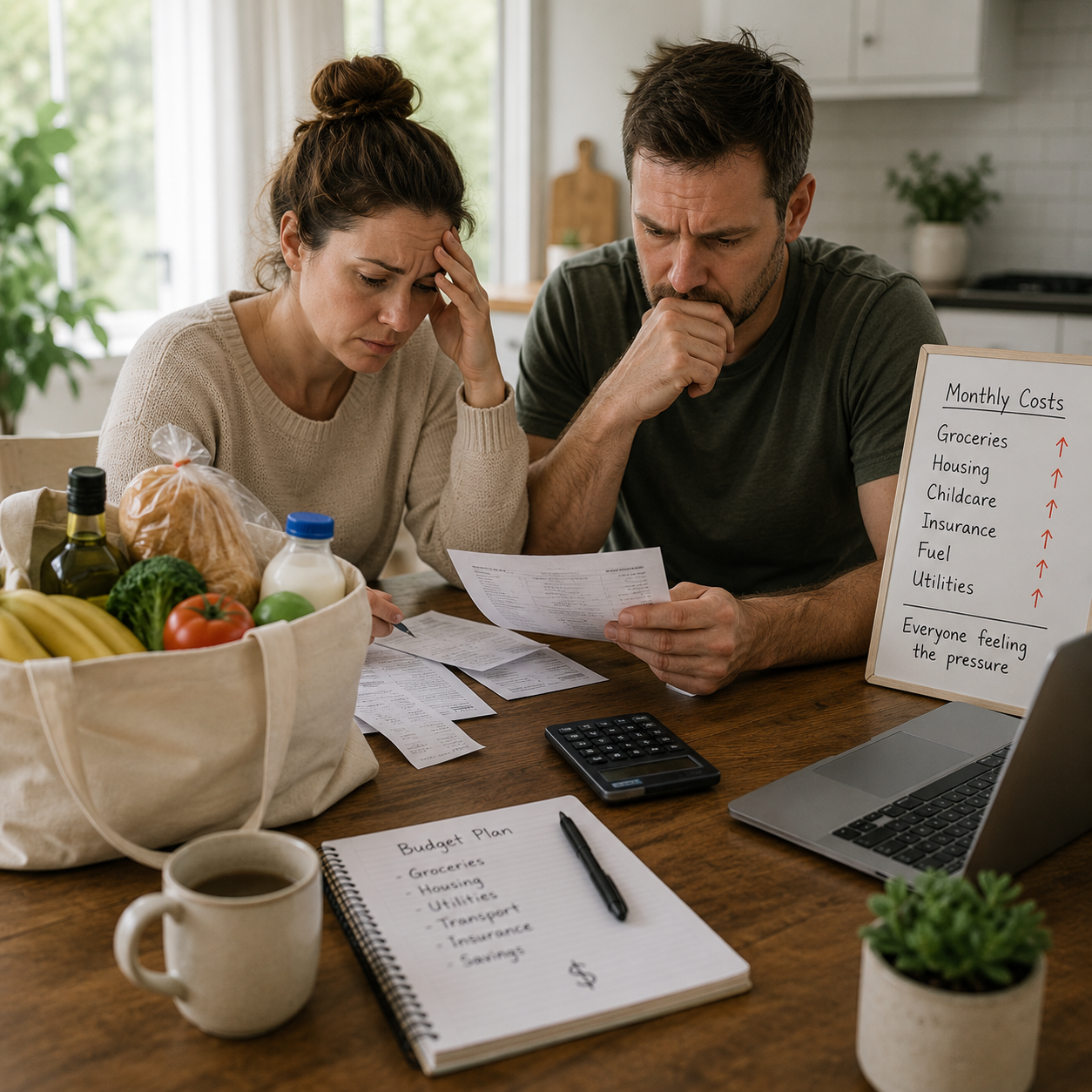

Many everyday costs now demand more attention.

Cost of living pressure can come from groceries, housing, childcare, insurance, interest rates, fuel prices, utilities, and the ongoing emotional load of financial decision-making.

When costs increase across several areas at once, people often need better structure, clearer priorities, and practical steps that work in real life.

Open each section for insights & actions.

Spending & Cash Flow

Debt & Lending

Housing Costs

Energy & Utilities

Government Support

Income & Work

Financial stress affects more than the numbers.

Focus & Energy

Financial pressure affects concentration and mental bandwidth at home & at work.

Relationships

Money stress can increase tension and make important conversations harder.

Decision-Making

Pressure can lead to reactive decisions instead of clear, intentional choices.

Confidence

People can lose momentum when they no longer feel in control of their finances.

Progress begins with behaviour, structure, & clarity.

Choose the type of support that fits your situation.

Financial Wellbeing in Your Workplace

Support your team with practical financial education that reduces pressure and builds confidence.

Personal Finances - Foundations & Horizons

Join a structured 6-week group program designed to help you make real financial progress. 1-hour Zoom call each week + recordings, resources, workbooks & support.

Individual Financial Coaching

Book a 90-minute Breakthrough Financial Coaching session. Tackle your biggest financial challenge. Walk away with practical steps & a clear path forward.

Tools, checklists, and guides.

The Resource Library is where you will find practical financial wellbeing tools, ebooks, worksheets, and guides designed to support everyday progress.

Practical and easy to apply.

Grocery resets, spending plans, debt repayment tools, money conversation guides, and cost of living checklists can all live here over time.

You don't need to solve everything at once.

A few practical changes, better structure, and clearer decisions will create real financial progress over time.